The Big Ideas of Investing

Introduction

Just like you, I’ve read lots of “how to” investing books over the years, and just like you, (I imagine) I feel most of them are repeats of one another, and actually not that helpful. Obviously, there are some books that shine through, and those that are considered must-reads (like Commons Stocks and Uncommon Profits by Fisher, or The Intelligent Investor by Graham), but to to make the lessons more applicable I think the knowledge has to be distilled, and processed individually.

So, this summer when I listened to an episode of This Week in Intelligent Investing, run by the very talented John Mihaljevic with Phil Ordway & Elliot Turner as co-hosts, called The Big Ideas of Investing, something really clicked. During the first ~28 minutes of the show, Phil recites a list that was given to all of his students at the end of his M.B.A. class at Kellogg School of Management at Northwestern University. This is a list with basic principles of investing that every investor should at the very least think through - and hopefully understand.

So, what I did was that I took Phil’s list, which he kindly shared on Twitter a while back, printed it out, took a scissor and separated all ideas from each other, and then placed them in three different piles. I named the first pile Learning, the second one Psychology & Philosophy, and the third one Tools & Principles. A few of the ideas I threw away completely (some were, or felt like, duplicates, some were too precise), or edited, and some I added myself.

The idea here is obviously not to say that “this is how you become a great investor”, or that I for that matter understand every part of it. It should be seen as more of a study list, or food for thought if you will. It should be applicable to everybody (one step at a time), and hopefully feel evergreen ten year down the line. Here it goes.

I. Learning

↠ Think for yourself

- Figure it out. Don’t stop asking “why?” until you have the real answer.

↠ Know what you don’t know

- Avoiding stupidity - or being less stupid than everyone else – is often a better path to success than brilliance.

- Overconfidence is deadly.

- Have the courage to declare something too hard or unknowable, and vice versa; have the courage to act when something is well understood and attractive.

- “It is remarkable how much long-term advantage people like us have gotten by trying to be consistently not stupid, instead of trying to be very intelligent.” - Charlie Munger

↠ Ask yourself:

- Who doesn’t know that?

- And then what?

↠ Genuine curiosity is the most powerful tool an investor can have

- Most great investors act like bright, relentless, highly caffeinated investigative journalists.

- There are diminishing returns to research, but most people err on the other side by instead cutting corners.

“Follow your passion. That’s the most important thing. And, read like crazy. And be curious. About everything.” - Chuck Akre (Invest Like The Best)

↠ Read as much as possible

- Track and measure what you read.

- Go to bed a little wiser each night.

- Learn something every day.

↠ Never assume anything

- Turn every page.

- Trust, but verify.

- The best way to solve a problem is often by looking at it backwards (i.e. Inversion).

- Think in probabilities.

- There are no certainties.

↠ Remove ignorance step-by-step, every day

- Always look for blind spots.

- Read Fooled by Randomness (Nassim Nicholas Taleb)

- Read Thinking, Fast and Slow (Daniel Kahneman)

“The first principle is that you must not fool yourself — and you are the easiest person to fool.” - Richard Feynman

↠ Scramble out of mistakes as quickly as possible

- Keep an investing journal.

- Be wary of The Sunk Cost Fallacy: “The decision to invest additional resources in a losing account, when better investments are available, is known as the sunk-cost fallacy, a costly mistake that is observed in decisions large and small.” The trick, says Kahneman, is to avoid “the escalation of commitment to failing endeavors” and to “ignore the sunk costs of past investments when evaluating current opportunities.”

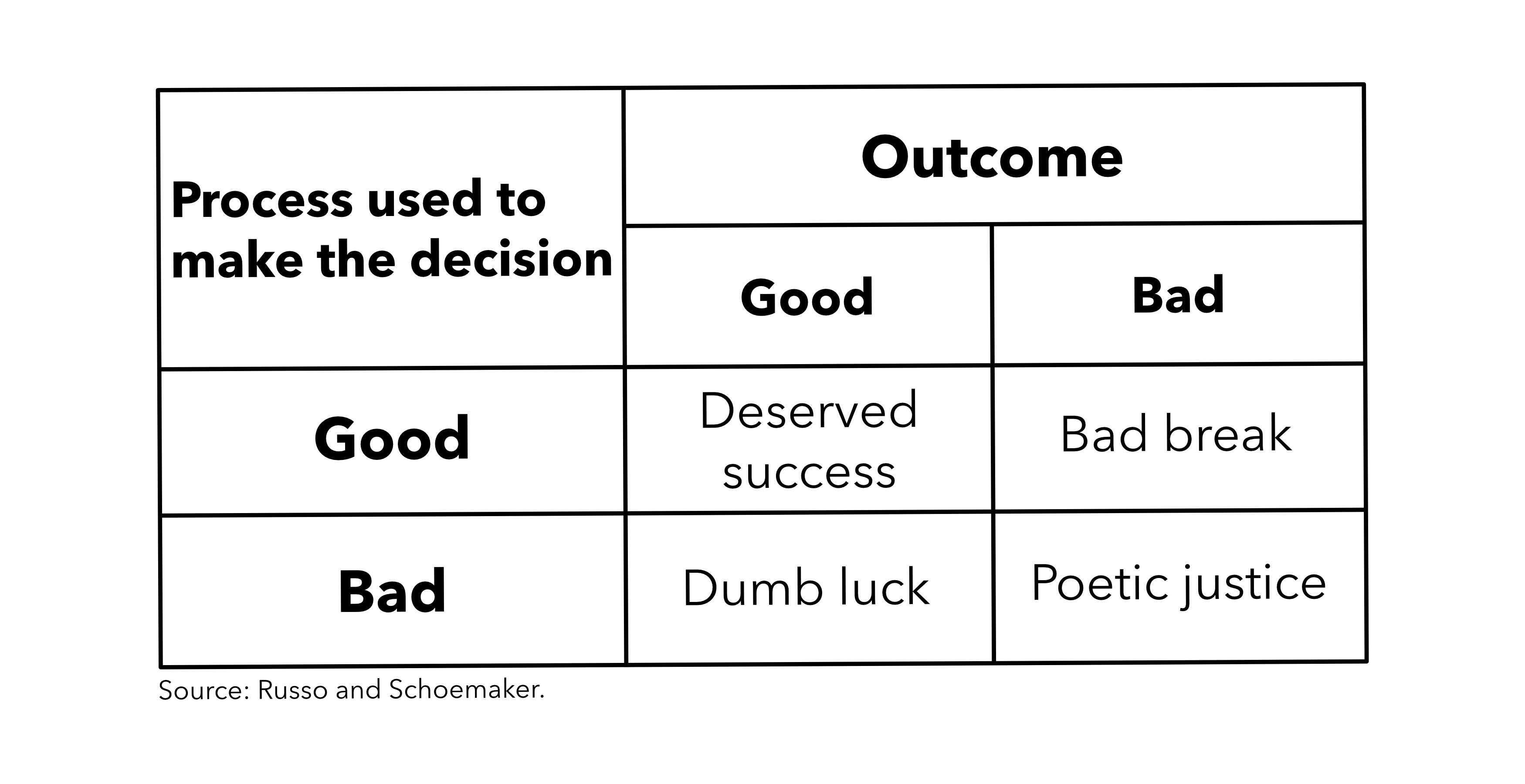

↠ Learn to differentiate between Process vs. Outcome

- “Individual decisions can be badly thought through, and yet be successful, or exceedingly well thought through, but be unsuccessful, because the recognized possibility of failure in fact occurs. But over time, more thoughtful decision-making will lead to better overall results, and more thoughtful decision-making can be encouraged by evaluating decisions on how well they were made rather than on outcome” - Robert Rubin (Harvard Commencement Address)

“Choosing individual stocks without any idea of what you're looking for is like running through a dynamite factory with a burning match. You may live, but you're still an idiot.” - Joel Greenblatt

↠ Knowing too little is obviously dangerous, but knowing too much can also be dangerous if it forces attention away from what matters

↠ There is such a thing as a dumb question

- With one exception; lazy questions that could be easily looked up or answered elsewhere show lack of effort, awareness, and consideration, which is dumb.

II. Psychology & Philosophy

↬ Investors value companies

- The future value of a company is the sole focus.

- Securities are simply a means for making an investment in a company.

↬ Many great mistakes begin by forgetting what one is trying to accomplish

- Investing is the art of laying out money today to get that money back in the future, plus a satisfactory return. Everything else is secondary to this aim.

- The value of any financial asset is the discounted present value of future cash flows. Everything else (multiples for example) is a derivative of this concept.

- Some cash flows are more reliable than others.

"A DCF to us is sort of like Hubble telescope - you turn it a fraction of an inch & you're in a different galaxy" - Curtis Jensen

↬ Incentives matter, almost to the exclusion of everything else

- Are the manager’s in the same boat as you?

- Businesses are dynamic, ever-changing, and run by real human beings.

- Read about Charlie Munger and Warren Buffett.

- Read Influence (Robert Cialdini)

↬ Temperament and behavior are far more important than IQ and analysis

- High-IQ investors have little if any advantage over above-average IQ investors if they can’t control their emotions.

- FOMO is a very real thing, especially in today’s information-packed world.

- Trust the process.

↬ The spread of excellence – also known as the paradox of skill – is real

- “The key is this idea called the paradox of skill. As people become better at an activity, the difference between the best and the average and the best and the worst becomes much narrower. As people become more skillful, luck becomes more important. That’s precisely what happens in the world of investing.” - Farnam Street

↬ Study history to better understand today

- "Whoever wishes to foresee the future must consult the past; for human events ever resemble those of preceding times. This arises from the fact that they are produced by men who ever have been, and ever shall be, animated by the same passions, and thus they necessarily have the same results." - Machiavelli

↬ Reflexivity is real

“Reflexivity theory states that investors don't base their decisions on reality, but rather on their perceptions of reality instead. The actions that result from these perceptions have an impact on reality, or fundamentals, which then affects investors' perceptions and thus prices. The process is self-reinforcing and tends toward disequilibrium, causing prices to become increasingly detached from reality.” - Investopedia

↬ Data reflect the past

- Market prices reflect expectations about the future.

- “Quantitative insight is efficiently priced, qualitative insight is not.” - Pat Dorsey

- All the data is in the past, but all the value is in the future.

↬ Markets are capable of crazy, improbable things

- Size accordingly when betting against something that’s being fundamentally just “too crazy” - it can always become even more crazier. Always.

↬ There is nothing wrong with speculation per se, but never confuse it with an investment

- Speculators rely on future changes in price and often need ready buyers at that price to achieve a good outcome. Investors focus on future changes in cash/economic value and would own an asset regardless of available buyers.

↬ Big events or outsized results are almost always caused by an interplay of different factors

- Being able to differentiate between process and outcome, as mentioned before, is hard but crucial.

↬ Allocating capital requires the humility to prepare and the arrogance to act

↬ Longevity is crucial

- Take risk, but make sure it’s managed properly (i.e. size accordingly).

- Never bet the farm. Never. Protect your downside.

- Be wary of hubris when things go well.

- “Any poker player knows that it is not how many hands you win that matters, it’s how much you win when you win, and how much you lose when you lose.” - Lee Freeman-Shor (The Art of Execution)

Morgan Housel’s list (The Psychology of Money), of things Warren Buffett didn’t do to achieve his success (parentheses mine):

Get carried away with debt (although, he have used leverage)

Panic and sell during the 14 recessions he’s lived through.

Sully his business reputation.

Attach himself to one strategy, one world view or one passing trend.

Rely on others’ money (a qualified truth, since he managed others’ money during the partnership years).

Burn himself out.

↬ Be wary of Ambiguity Aversion

- “One of the reasons people hold onto losing positions is fear of the unknown. If they sold out, the shares might rally, and they would miss out. It feels better to stick with a loss than to worry about a double-whammy.” - Lee Freeman-Shor

↬ Many aspects of investing are ideas that seem to contradict each other

- Many great failures – both investing and life in general – come from the inability to hold two ideas at once.

- “Strong opinions loosely held” - have a flexible mind.

III. Tools & Principles

↝ Valuation is not possible without a thorough understanding of a business’ competitive environment

- Crap in means crap out. If you don’t understand the market environment where the company operates, (i.e. what’s actually driving, or could hinder, their growth) or the unit economics, your model won’t be of much use.

↝ Pricing and valuation are distinct exercises and not to be confused

↝ Multiples are a blunt, crude proxy for a real valuation process

– A way to quickly price an asset, not an (effective) way to truly value it.

- Some multiples are better than others, and some are outright unhelpful.

↝ The best valuation processes leave plenty of room for error and randomness

↝ Human + machine is more powerful than human or machine in isolation

- Try to de-human some parts of your process to avoid human bias.

- Stop-losses, or at least automatic reminders at specific price levels, can spare you a lot of trouble. Recheck your story when the market goes against you.

- Winners make small mistakes, losers make big mistakes.

"Human managers process information spontaneously using poorly thought-out criteria and are unproductively affected by their emotional bias. These all lead to suboptimal decisions. Imagine what it would be like to have a machine that processes high-quality data using high-quality decision-making principles/criteria." - Ray Dalio (from his book Principles)

↝ Earnings are a matter of opinion

- Cash drives economic value (and is much harder to fudge).

- Financial statements originally focused on liquidity and solvency; many financial statements today focus instead on earnings or, worse, “adjusted” earnings or, worst of all, adjusted proxies for earnings.

- Balance sheets are more useful than cash flow statements, and cash flow statements are more useful than income statements.

↝ The “cost of capital” is determined by your opportunity cost

- Precise calculations of the cost of capital are useless.

↝ The best valuation processes follow a particular order

- Start with the materials a company is required to disclose (regulatory filings, audited financials, etc), and study the business – not the valuation.

- Then review what a company chooses to disclose (press releases, presentations, conference calls, etc).

- Only consider opinions at the end, and then seek out opinion on both sides with an emphasis on disconfirming evidence.

- Bias is inherent and unavoidable; don’t succumb to an anchor before the real work has even begun (remember the utility of a blind valuation).

- Valid judgments can only be made after gaining enough perspective to argue the other side at least as well as its proponents.

↝ The valuation process results in a range, not a number

- “Essentially all models are wrong, but some are useful.” - George Box

↝ Conditions change, but principles remain

- Dare sticking to your own process, and only iterate when needed.

- Try to create a personal investment process that can be replicated successfully >5 out of 10 times, and then let time do the work.

“We can’t change what’s going on out there, that’s the wind blowing.” – John Earl Shoaff

Thanks for reading! Here’s the original doc by Phil Ordway.